Innovative Lending Strategies for Banks, Credit Unions, and Fintechs

The most innovative lenders in 2026 are rethinking how lending products are built, distributed, and serviced from the ground up.

This shift is showing up in real ways. Product cycles are shrinking. Distribution is moving closer to the point of need. Servicing is becoming more automated, more predictive, and more responsive to borrower behavior. Institutions that move quickly are capturing share while others are still working through outdated systems and assumptions.

This post gives operators a practical look at what's actually changing inside leading banks, credit unions, and fintech organizations, and what you can start doing about it today.

Why lending innovation isn't optional anymore

Innovation in lending is now tied directly to growth. Digital lending innovation is no longer about adding new features. It’s about rethinking how products are built, delivered, and managed.

Institutions that move quickly are capturing market share while others work through outdated infrastructure and assumptions. In fact, fewer than 1 in 10 bank leaders consider their organization at the leading edge of digital transformation, according to a Gresham Tech report. The report also found 18% of banks admitted they were lagging behind while 44% were working to catch up on digital transformation.

9 innovative lending strategies redefining the industry in 2026

The following 9 strategies reflect how leading financial providers are modernizing their infrastructure and evolving their approach across origination, servicing, and product design.

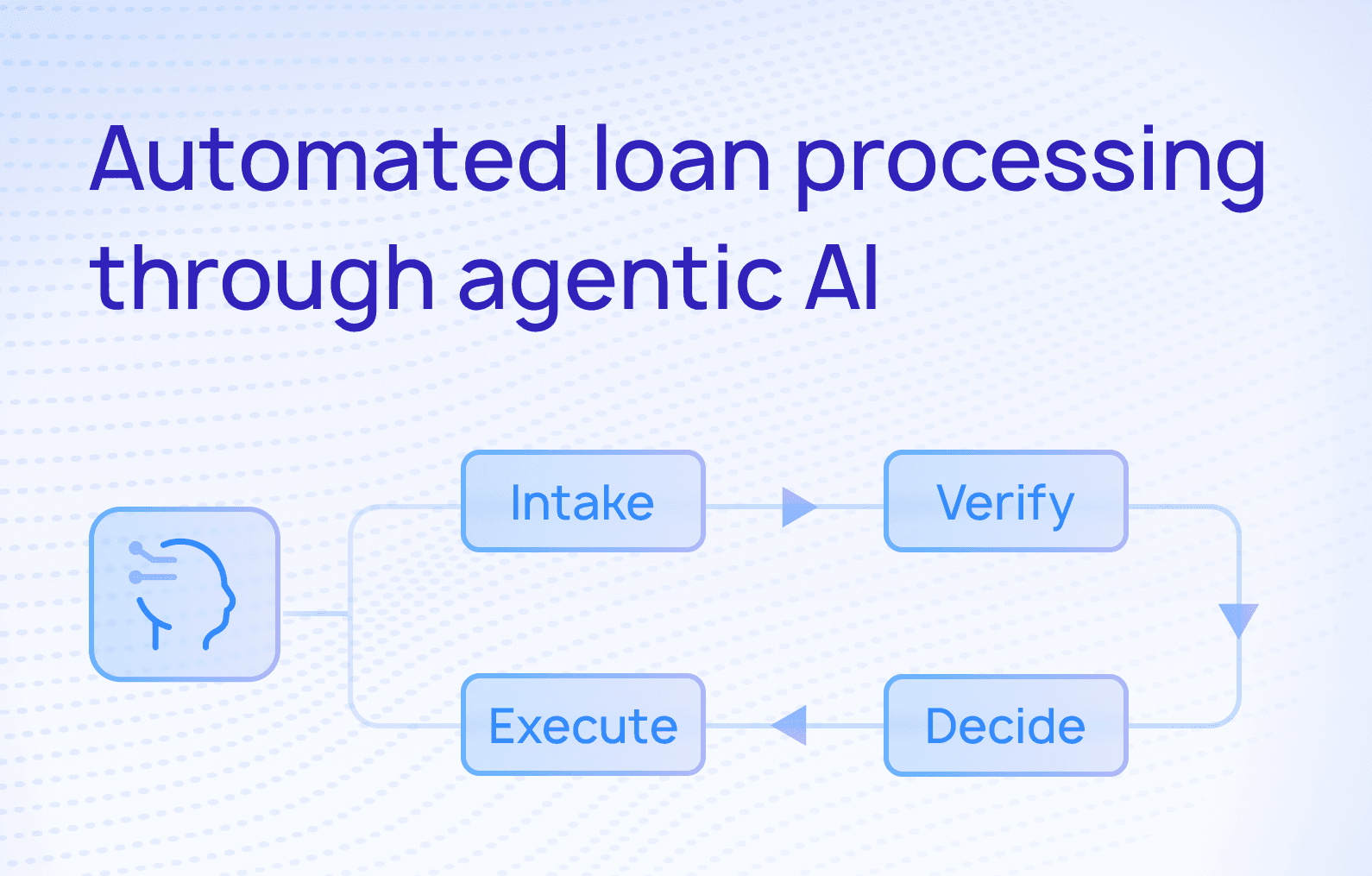

1. Scale servicing without scaling headcount

Servicing costs continue to rise while borrower expectations for responsiveness keep increasing. Agentic loan servicing can enable institutions to scale operations without adding headcount while maintaining consistent service quality.

AI-driven agents can now handle routine and complex servicing tasks autonomously: payment processing, borrower communications, dispute handling, and exception management, all without constant human oversight. This is what agentic loan servicing makes possible.

Executing this well requires orchestration layers that can integrate with core systems, as well as access to structured servicing data. Model Context Protocol (MCP) integrations are emerging as a key enabler for connecting AI agents directly into operational workflows.

2. Launch new loan products in weeks, not quarters

As market conditions shift more frequently, institutions that can respond quickly to rate changes or borrower demand spikes gain a measurable advantage in both acquisition and retention.

An API-first infrastructure allows lenders to configure and launch new loan products in weeks instead of months. Product terms, pricing, and workflows can be adjusted without heavy engineering cycles.

To support this approach, lenders need modular systems with configurable product engines and well-documented APIs. The ability to test and iterate on products quickly becomes part of the competitive playbook.

3. Meet borrowers where they already make decisions

Distribution has become a primary battleground for lenders. Borrowers increasingly expect financial services to appear within their existing workflows rather than requiring a separate application process. In fact, integrating point-of-sale financing directly into the checkout flow can boost cart conversion rates by up to 30%, according to Future Market Insights.

Embedded lending places credit directly within the platforms borrowers already use, such as ERPs, marketplaces, and vertical SaaS tools. Origination moves closer to the moment of need, reducing friction in the borrowing process.

Delivering embedded lending requires partner-ready APIs, flexible underwriting models, and the ability to integrate into third-party ecosystems. It also requires operational readiness to support higher volumes of smaller, context-driven loans.

4. Compete at the point of sale with Buy Now, Pay Later

Fintechs have spent years capturing point-of-sale financing that traditionally belonged to banks and credit unions. Buy Now, Pay Later (BNPL) products give traditional lenders a way back into that moment, offering installment options at checkout without sending borrowers to a third-party provider.

Execution here depends on product flexibility. BNPL terms vary widely across merchants, purchase sizes, and borrower profiles. Lenders need configurable product engines that can handle that variation without custom builds for every use case.

Institutions that can launch and adapt BNPL programs quickly will be well-positioned to compete in a space that fintechs have owned by default.

5. Turn every credit line Into a multi-product experience

Borrowers want flexibility without managing multiple accounts or providers. By unifying credit cards and installment lending onto a single platform, lenders can expand product surface area while simplifying infrastructure.

These unified credit programs enable capabilities like loan on card programs, hybrid repayment structures, and shared credit lines across products.

Execution depends on having a system that supports multiple credit products within one framework. This includes shared data models, unified servicing, and consistent compliance controls across product types.

6. Underwrite based on what borrowers actually do

Transaction-level decisioning is gaining traction in 2026 as lenders look to expand access while managing risk. Thin-file and underbanked borrowers become more reachable when underwriting reflects actual financial activity.

This approach looks beyond traditional credit scores to evaluate financial behavior more accurately using real-time spending and cash flow data.

To implement this, institutions need access to permissioned transaction data, along with analytics capabilities that can process and interpret that data quickly. Open banking integrations play a central role here.

7. Price every loan for the person, not the product

Today, borrowers expect personalized offers, and lenders need tools to manage margin and risk dynamically. Relying on static pricing models limits the ability for lenders to move away from one-size-fits-all rate structures.

Real-time dynamic pricing allows lenders to adjust loan terms in real time based on borrower risk signals, market conditions, and portfolio performance. Rates and offers can shift as new data becomes available.

Supporting this strategy requires real-time data pipelines, pricing engines, and governance frameworks to ensure consistency and compliance. It also requires alignment between risk, product, and finance teams.

8. Fund loans at the speed borrowers expect — instantly

Instant or same-day loan disbursement has become a baseline expectation in many lending segments. Borrowers want access to funds immediately after approval.

In 2026, speed of funding is directly tied to borrower satisfaction and conversion rates. Delays in disbursement create drop-off and reduce trust. For example, 90% of consumers say they would prefer to receive disbursements instantly if given the choice, according to a report produced by PYMNTS and The Clearing House.

Executing this requires integration with modern payment rails, such as RTP and FedNow, along with systems that can trigger funding events automatically. It also depends on having end-to-end digital workflows that eliminate manual bottlenecks.

9. Get ahead of delinquency before it costs you

Finding ways to mitigate loan delinquency before it happens is gaining importance in 2026 as economic uncertainty continues to affect borrower stability. Early intervention improves retention and reduces charge-offs while supporting compliance expectations.

Proactive hardship programs identify at-risk borrowers early and offer flexible repayment options before missed payments occur. This includes payment deferrals, restructuring, and tailored support.

To implement this effectively, lenders need predictive analytics, configurable program management tools, and the ability to adjust loan terms dynamically. Communication workflows also play a critical role in engaging borrowers at the right time.

What the most innovative lenders have in common

Across all 9 strategies, a fintech innovation pattern emerges. Adaptability. The most innovative lenders are building around flexibility, speed, and integration. They're investing in infrastructure that lets them configure products quickly, connect to external ecosystems, and operate in real time.

They also treat lending as a continuously evolving system rather than a fixed set of products. This mindset allows them to respond to market shifts without rebuilding from scratch each time. To compete in 2026, the most innovative lenders must be able to adapt quickly and execute consistently.

See how LoanPro can help you put these innovative lending strategies into action. Request a demo today.