Credit risk management: A guide for modern credit providers

Credit has always been about trust — can borrowers pay back any loans or credit? But, the ability to assess and grant trust is being tested at a higher scale and speed than ever before.

Credit risk management processes need to operate in a world of real-time decisions, volatile macro conditions, evolving regulation, and customers who expect instant approvals without friction. Traditional credit risk management strategies are no longer enough to win in today’s market.

In this guide, we’ll outline:

- What is credit risk management?

- Why traditional credit risk frameworks are no longer enough

- The modern credit risk management process

- Moving from manual reviews to automated guardrails

- Credit risk management best practices for 2026

What is credit risk management?

Credit risk management is the process of identifying, measuring, and controlling the risk that a borrower won’t repay money they owe on time or even at all. Modern credit risk management is not just about preventing losses. It’s about enabling your credit business to grow with confidence.

The most successful lenders, credit providers, and financial institutions are not the ones that seek to avoid risk entirely. Instead, they are the ones that can balance safety and growth — taking enough risk to make money, but not so much that it threatens the business. To assess credit risk, lenders will evaluate the likelihood that a borrower will default on their debt obligations by looking at a combination of the borrower's financial history, current circumstances, and ability to repay with broader economic factors that might affect their future capacity to pay back a loan.

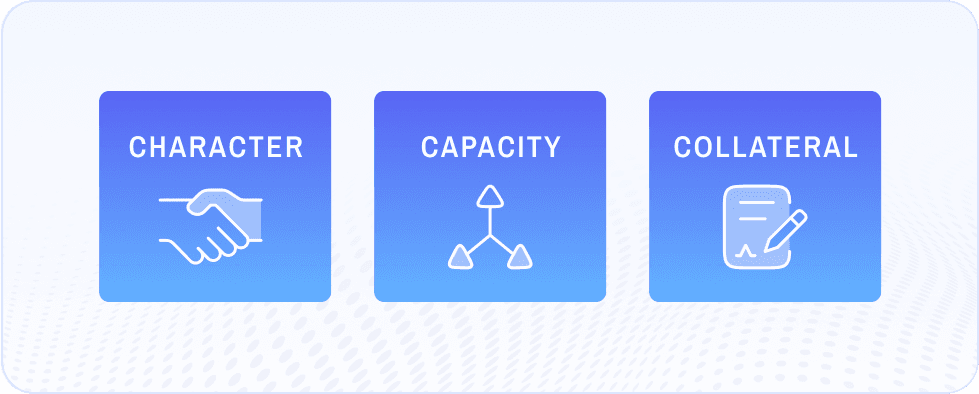

The 3 C’s of traditional credit risk management

We’ve written before about the widely-used framework of the 3 C’s of credit — character, capacity, and collateral — for evaluating potential borrowers’ creditworthiness. Let’s look at each of these in more detail:

Character: This looks at a borrower’s trustworthiness to repay a loan. It is often determined by positively identifying the individual and then, looking at their financial history and behavior patterns.

Capacity: This looks at a borrower’s likely ability to repay the loan. Several consideration factors to determine this can include a person’s income and expenses, any pre-existing debt, and how the borrower’s ability to pay may evolve in the future.

Collateral: This refers to any assets or savings that could be used to repay the loan. You’ll sometimes see this referred to as capital and collateral. While not every credit product requires specific assets to be pledged to secure a loan, assessing a borrower’s capital and collateral can help mitigate credit risk.

Why traditional credit risk management frameworks are no longer enough

Traditional credit risk management frameworks were built for a slower paced, more stable, and more predictable world. Today, lenders are dealing with marketplaces that move faster, are more interconnected, and flooded with new types of data, such as cash flow or alternative credit data.

Just look at the 2008 financial crisis as one example of these old approaches starting to show their cracks. The financial industry’s reliance on backward-looking accounting methods masked massive risk. And, that was nearly 20 years ago now.

Here’s a few key reasons why traditional credit risk management strategies are no longer enough:

Reliance on backward-looking data: Traditional credit risk models lean on historical financials, credit scores, and long reporting cycles. In today’s world, a borrower’s risk profile can change in weeks or days, not quarters or years. By the time the data shows a problem, it’s often already too late.

Economic stability that no longer exists: Classic frameworks were designed around “normal” economic cycles. But recent years have brought sudden market shocks, supply chain disruptions, rapid rate changes, and even a global pandemic. These types of events break models that assume gradual change.

New types of borrowers: Gig workers, digital-first businesses, fintech customers, and platform-based companies don’t fit neatly into standard balance sheets or income verification processes. And, the rise of cash flow underwriting provides a better way for modern lenders to evaluate a borrower’s ability to pay back a loan based on alternative credit data.

Slow, manual processes: Many traditional credit risk management processes involve manual reviews, static scorecards, and periodic backward-looking reassessments. This slows down decision making and makes it hard for lenders to effectively scale and compete in a digital-first ecosystem.

Traditional credit risk frameworks simply can’t keep up with the speed, complexity, and volatility of today’s marketplace. Instead, modern credit risk management best practices focus on real-time data, automation, and forward-looking thinking to more effectively assess and mitigate credit risk.

The modern credit risk management process

By contrast, a modern credit risk management process is dynamic, data-rich, and continuous. It is designed to enable lenders to adapt in real time, not just approve loans and look back later. Modern credit risk management platforms deliver:

Continuous data visibility

Modern frameworks pull from multiple data sources — traditional and alternative credit — on an ongoing basis to provide a more complete, accurate picture of a borrower’s creditworthiness. This can include transaction data, behavioral signals, market indicators, and external risk events, not just static financial statements.

More importantly, modern credit platforms like LoanPro enable lenders to create a centralized, single source of truth, securely housing all of their data and processes in a system that grants them unprecedented visibility and control over how they manage their portfolio.

Beyond static models for credit risk assessment

Instead of focusing solely on static models or past behaviors, modern credit risk assessments evaluate multiple factors simultaneously:

- Credit history analysis examines past payment behavior, outstanding debts, and credit utilization patterns. This historical data provides the strongest predictor of future payment behavior for most borrowers.

- Income and employment verification ensures borrowers have sufficient cash flow to support new debt payments. Debt-to-income ratios help lenders understand whether proposed payments fit within the borrower's overall financial capacity.

- Collateral evaluation provides additional security for secured loans, though lenders must consider potential depreciation and recovery costs.

In addition, modern credit risk management best practices should factor in scenario analysis, early-warning indicators, and predictive models to better understand and evaluate potential risks.

Real-time decisioning

Instead of slow, manual reviews and approvals, modern credit risk platforms enable risk insights to feed directly into workflows for faster credit approvals and dynamic pricing and terms. Modern credit providers are turning to an integrated decisioning solution that can improve their accuracy, streamline their approvals, and keep their data visible. For instance, LoanPro’s decisioning engine integrates into the account lifecycle to cut down on approval wait times without compromising accuracy or efficiency.

Ongoing credit risk monitoring

Modern credit risk management strategies don’t wait for scheduled reviews or delinquency to show up. They continuously watch borrower behavior, exposure, and external signals, looking for change, not just absolute risk. To do this, lenders need live data feeds, strong early-warning indicators, dynamic risk scoring and segmentation, and automated alerts and workflows.

LoanPro’s Smart Verify tool offers real-time data access, automates compliance checks, and enables this type of ongoing monitoring to reduce risk throughout the credit lifecycle.

Bottom line: Instead of waiting for something to happen, ongoing credit risk monitoring looks at what is changing now and what should be done about it. This enables lenders to intervene earlier, mitigate credit losses, create a better borrower experience, and build more resilient credit portfolios.

Proactive delinquency management

Loan delinquency management refers to any processes that lenders use to encourage repayment when borrowers fall behind on their debt. This can range from quick due date reminders to repossessions.

Instead of waiting for a borrower to default, modern credit providers focus on proactive measures that can help prevent loan delinquency before it happens. This starts with credit risk assessments to prevent approving a loan that will have a bad outcome. But, it also includes proactive communications during the loan origination process to help borrowers understand the consequences of repayment and delinquency. And, regular reminders throughout the account lifecycle can help ensure repayment remains a priority.

Finally, proactive delinquency management can also mean ensuring the payment process is simple, secure, and streamlined. Case in point: Best Egg, a leading financial confidence platform that provides flexible solutions to help people with limited savings confidently navigate their everyday financial lives, turned to LoanPro to help optimize its payment and collection processes.

Now, Best Egg uses LoanPro’s Secure Payments product to handle 80% of its payment processing needs. Secure Payments also enables Best Egg to deliver payment flexibility to its borrowers, reducing default rates even further across its portfolio.

Moving from manual reviews to automated guardrails

One of the most important differences in a modern credit risk management framework versus traditional strategies is shifting from manually checking individual decisions to designing the rules, thresholds, and controls to guide automated processes at scale.

Instead of case-by-case approvals, pre-defined risk boundaries can set clear risk thresholds to enable automated approvals. In this model, manual reviews become the exception based on escalation logic rather than the norm.

Instead of relying on human memory and informal judgments, automated guardrails create explicit rules with transparent decision logic and consistent enforcement.

Instead of manual intervention processes after something looks wrong, automated guardrails can proactively prevent risk by capping exposure automatically, blocking risky behaviors in real time, and setting warning triggers so lenders can intervene early.

Markets move too fast and portfolios are too big for humans to be involved in every step. With the right automated guardrails, modern credit providers can scale safely, reduce inconsistencies, and ensure they meet compliance requirements easily every time.

Want to see these strategies in action? Leading lenders using LoanPro have reduced credit losses by 38%. Download our one-pager to see the full impact of modern credit risk management.

Credit risk management best practices for 2026

Macroeconomic volatility, regulatory pressures, changing customer behaviors and demands, cash flow instability, technology innovations, and more. These are just a few of the biggest factors that will shape credit risk management this year.

As these risks become increasingly connected and as conditions continue to evolve rapidly, modern credit providers should consider a few key best practices for 2026:

-

Treat credit risk as a growth enabler. Instead of simply taking actions to reduce risk, smart risk teams will focus on how to grow safely.

-

Move from periodic reviews to continuous monitoring. We’ve already talked about how periodic reviews are no longer sufficient in today’s dynamic credit environment. If you aren’t already, now is the time to establish continuous data visibility and ongoing monitoring processes.

-

Strike the balance between speed and discipline. Customers expect and demand instant approvals for credit. Slow, manual processes will not only irritate customers, it will make them turn elsewhere. Establish real-time decisioning with clear, automated guardrails.

-

Blend traditional and alternative credit data. Credit scores and cash flow data should be viewed as complementary data sets that can help create a more complete picture of a potential borrower — particularly if that borrower has a thin credit file. Traditional credit scores focus on past credit behavior, showing a borrower’s willingness to pay back loans and credit based on their payment history. On the other side, cash flow data provides lenders with real-time insights into a borrower's actual income, spending, and savings. This shows their ability to pay, not just their willingness to pay.

-

Build strong early-warning and intervention playbooks. The best way to manage loan delinquency is to prevent it from happening in the first place. The best credit providers will define clear risk signals and actions to take to proactively engage borrowers before it’s too late.

-

Ensure compliance and governance remain non-negotiable. With increased automation and the use of artificial intelligence, ensuring every decision is explainable is more important than ever. Invest in embedded compliance tools that automate compliance and regulation so you can focus on driving growth for your business.

These best practices provide a strong foundation for 2026, but credit risk continues to evolve. To help you stay ahead of developing trends, watch our on-demand webinar with industry expert Kevin Moss, the former Chief Risk Officer at SoFi and Wells Fargo, to hear his take on credit risk management in 2026, including how to defend against fraud, defaults, and the student loan default cliff