Embedded lending: What it is and how it works in 2026

Over the past decade, financial services have moved steadily closer to the moments where customers need them most. Payments became embedded within digital experiences first. Banking capabilities followed close behind. Now, lending has entered the same phase of transformation.

Instead of a separate action, credit is becoming part of the customer journey, delivered at the point where financial decisions already occur.

This model, known as embedded lending, is changing how loans are distributed, originated, and serviced. Industry projections show the embedded finance market is expected to reach $7.2 trillion in size by 2030, with lending representing one of the fastest growing opportunities within that ecosystem.

To understand why embedded lending is gaining momentum, let’s dive deeper into how it relates to broader concepts and how it works. In this post, we’ll explore:

- What is embedded lending?

- Embedded lending vs. embedded finance

- Embedded finance vs. Banking-as-a-Service

- How embedded lending actually works in practice

- Is embedded lending regulated?

- The embedded lending network in 2026

- Who's using embedded lending?

- Why platforms are embedding lending now

What is embedded lending?

Embedded lending refers to the delivery of loan products directly within a non-financial platform or digital experience. Financing is offered at the moment a customer completes a transaction, manages operations, or makes a purchase decision. This allows borrowers to access credit without leaving the environment they are already using.

Instead of navigating to a lender’s website or an online application portal, customers encounter financing options inside software platforms, marketplaces, or service ecosystems. The platform facilitates the experience while regulated lenders provide capital and manage loan programs behind the scenes.

Embedded lending already appears across a growing number of everyday digital experiences. Common examples of embedded lending include:

- Ecommerce platforms that offer merchant financing

- Equipment vendors who provide Buy Now, Pay Later installment financing options at checkout

- Vertical SaaS platforms enabling working capital for small businesses

- Marketplaces that offer seller or contractor advances

In short, embedded lending changes where lending begins, shifting distribution closer to everyday economic activity.

Embedded lending vs. embedded finance

Embedded finance describes the integration of financial services into non-financial platforms. These services may include payments, accounts, insurance, cards, or lending capabilities delivered within a digital experience.

Embedded lending represents just one component within the broader embedded finance landscape. While embedded finance spans multiple financial products, embedded lending focuses specifically on delivering credit products such as installment loans, Buy Now, Pay Later solutions, lines of credit, or merchant financing within platform experiences.

This distinction becomes important as lending introduces lifecycle requirements that extend beyond transactions, including repayment management, servicing, compliance oversight, and ongoing customer engagement.

Embedded finance vs. Banking-as-a-Service

Embedded finance represents the customer-facing experience, while Banking-as-a-Service (BaaS) provides part of the underlying infrastructure that makes those experiences possible.

BaaS solutions enable licensed financial institutions to provide regulated banking capabilities through APIs that third parties can integrate into their products. BaaS providers connect platforms with banking infrastructure such as accounts, payments processing, or lending capabilities.

Embedded finance builds on this BaaS foundation by integrating those financial capabilities directly into digital platforms where customers already operate. Through embedded finance, platforms can offer payments, accounts, cards, or lending experiences as part of their core product experience rather than directing users to external financial institutions.

Together, these models allow financial services to be distributed through software platforms while regulated institutions continue to provide licensed banking and lending functions behind the scenes.

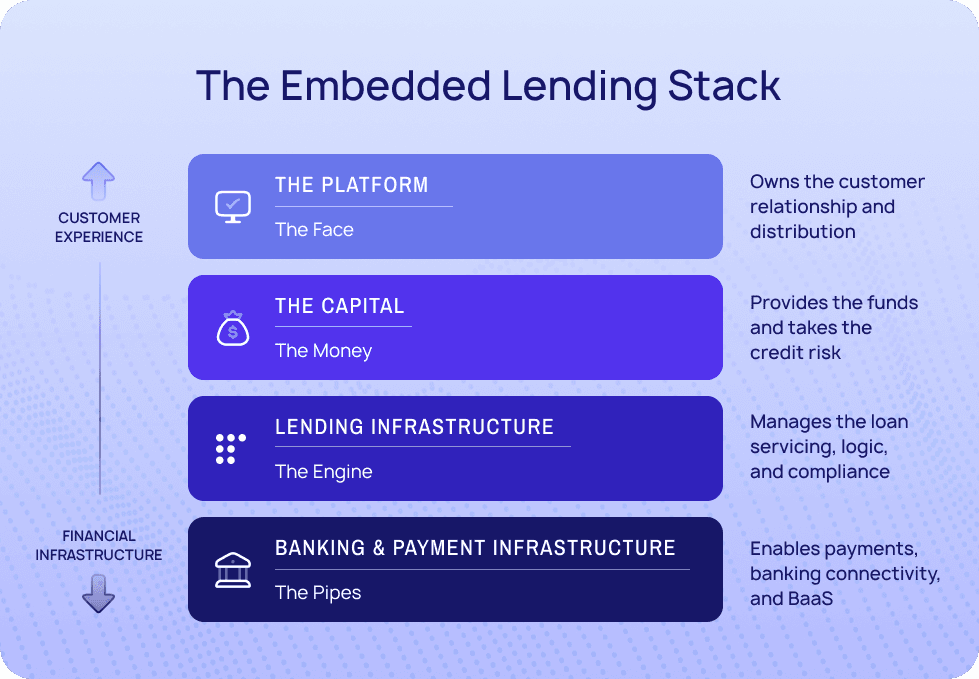

How embedded lending actually works in practice

Embedded lending operates as the credit component of embedded finance, supported by Banking-as-a-Service infrastructure. For example, a typical embedded lending program brings together several participants:

- The platform or end company integrates financing directly into its customer experience and owns distribution, engagement, and customer relationships.

- The financial institution or lender originates loans, provides capital, and assumes credit and regulatory responsibility for lending activities.

- Loan management platforms support product configuration, origination workflows, servicing, repayment processing, compliance tracking, and lifecycle management throughout the life of the loan.

- Banking and payment infrastructure, including Banking-as-a-Service providers, enables money movement, account connectivity, and access to regulated banking capabilities required to operate embedded lending programs.

When these components operate together, financing can be offered at the point of need while remaining connected to regulated banking infrastructure and ongoing loan operations.

From a borrower’s perspective, the experience appears seamless. Financing is presented within the platform they already use, applications occur within existing workflows, and repayment continues through familiar digital channels. Behind the scenes, multiple systems coordinate to manage compliance, capital flow, and servicing responsibilities across the life of the loan.

Embedded lending succeeds when customer experience, capital, loan operations, and banking infrastructure operate as a coordinated ecosystem.

Is embedded lending regulated?

While embedded lending feels seamless to borrowers, lending remains a regulated financial activity. Embedded finance and embedded lending change how loans are delivered, while regulatory obligations continue to apply to the lending activity itself. The presence of an embedded lending experience does not change the regulatory accountability of the originating financial institution. Licensed financial institutions maintain responsibility for complying with applicable lending laws and supervisory requirements as they continue to originate loans and provide capital.

Because embedded lending programs involve multiple participants, compliance responsibilities become shared across the ecosystem. Financial institutions oversee underwriting standards, disclosures, and regulatory reporting. Platforms and technology providers support compliant program execution through automated workflows, controls, and operational oversight.

As embedded lending adoption expands, successful programs depend on clear coordination between platforms, lenders, and infrastructure providers to ensure compliance obligations are maintained consistently throughout the life of the loan.

The embedded lending network in 2026: Choosing the right partners

Embedded lending programs rarely rely on a single provider. Instead, they bring together platforms, capital providers, banking infrastructure, and loan management technology — each responsible for a different component of program execution. Selecting the right partners across this network has become a critical strategic decision.

When evaluating embedded lending partners, organizations should consider several key factors:

Lifecycle support beyond origination

Launching an embedded lending program represents only the beginning of the lending relationship. Loans must be serviced, modified, reconciled, and reported throughout their full lifecycle. Partners should support ongoing loan operations at scale, including repayment management, servicing flexibility, and evolving product structures as programs mature.

Flexibility across products and programs

Embedded lending often evolves quickly as platforms expand into new customer segments or financing models. Infrastructure should allow lenders and platforms to configure products, adjust terms, and launch new programs without extensive redevelopment. Modern lending infrastructure plays a critical role in enabling this flexibility. For example, LoanPro’s modern lending core is an API-first, configurable architecture, enabling companies to launch new products within two weeks.

Regulatory alignment across participants

Because responsibility spans multiple entities, embedded lending partners must operate within clearly defined compliance frameworks. Strong coordination between lenders, platforms, and infrastructure providers helps ensure regulatory obligations remain consistent across distribution channels and servicing environments.

Scalability across partner ecosystems

Early embedded lending programs may begin with a single platform relationship. Over time, organizations frequently expand into multiple partners, geographies, or lending programs. Technology and infrastructure decisions should support growth without requiring operational restructuring as programs scale.

Data visibility and operational control

Embedded lending introduces distributed customer experiences across external platforms. Maintaining unified data visibility into loan performance, repayment behavior, and portfolio health becomes essential for lenders managing risk and performance.

Who's using embedded lending?

Embedded lending spans a wide range of industries, as platforms look to integrate financing directly into the workflows where financial decisions occur. What began with ecommerce and merchant financing has expanded into vertical software platforms, healthcare ecosystems (including veterinary care), and specialized service providers.

In each case, financing becomes embedded within industry-specific customer journeys, helping customers act immediately rather than delaying decisions due to funding constraints or slow loan application processes.

Some of the most significant innovation in embedded lending is occurring in industries where financing needs do not fit conventional loan assumptions. Healthcare, education, and specialized services often involve uncertain costs, staged payments, or long decision timelines that require more flexible lending structures.

Future Family is a great example, transforming how American families access fertility treatment and financing. It is building a fundamentally new class of credit product that combines flexible financing options with personalized, expert care.

To support this model, Future Family embedded financing directly into its care platform, allowing families to access funding aligned with fertility treatment milestones while maintaining visibility and support throughout the process.

Launching and scaling this type of program required lending infrastructure capable of supporting flexible disbursements, integrated provider networks, and ongoing program iteration. Using LoanPro’s configurable loan management platform, Future Family moved from contract to live operations in four months and scaled from thousands to tens of thousands of patients while maintaining strong customer satisfaction outcomes.

The example illustrates how embedded lending increasingly enables organizations to build entirely new categories of credit products tailored to specific industries and customer needs.

As embedded lending expands across industries, organizations are discovering that success depends less on offering financing itself and more on the flexibility of the infrastructure supporting it.

See how LoanPro enables Future Family to transform fertility financing.

Why platforms are embedding lending now

Embedded lending adoption will continue to accelerate as platforms look for new ways to deepen customer relationships and expand the value they deliver within their ecosystems.

As SaaS platforms increasingly serve as systems of record for business operations and consumer activity, they are uniquely positioned to introduce financing at moments when access to capital directly influences decision-making.

The benefits of embedded finance for SaaS platforms and their customers are clear:

- Better customer experiences: Embedding financing directly within the platform reduces friction, shortens time to funding, and eliminates the need to navigate separate lending applications or providers.

- Data-driven underwriting: Platforms generate real-time operational and transactional data that can provide deeper insight into customer performance. When incorporated into lending decisions, this data supports more contextual underwriting and financing structures aligned with actual business activity.

- New revenue streams: Embedded lending enables platforms to participate more directly in the financial outcomes of their ecosystems. Financing programs can introduce new monetization opportunities while strengthening customer retention and long-term platform engagement.

- Greater financial inclusion: Embedded lending can also expand access to financing for businesses and consumers who may be underserved by traditional lending channels.

Together, these advantages are transforming embedded lending from an innovation initiative into a core platform growth strategy.

As embedded lending continues to mature, success depends on aligning customer experience, capital, and operational infrastructure in ways that allow programs to scale responsibly over time. Organizations building these capabilities today are helping define how lending will be delivered in the years ahead.