Digital transformation in lending has a deadline

For years, digital transformation in lending has lived comfortably on the roadmap. Important. Inevitable. But not urgent.

That window is closing.

A modern lending system is no longer a luxury or long-term investment. It’s a competitive advantage today, and very soon it will be the cost of staying in the game. The challenge is that many institutions do not fully understand the impact of delay. It shows up in servicing inefficiencies, manual processes, and legacy systems that quietly erode margin.

In 2026, standing still is no longer an option. The lenders who treat digital transformation as a future problem are already falling behind.

Customers are leaving for better digital experiences, new ones are harder to win, and market share is shifting. Loans are being approved in minutes and borrowing is happening digitally at scale. The gap between modern and legacy infrastructure is getting harder to ignore.

Most lenders know they're behind. Few are doing anything about it.

Many institutions already know they are operating with constraints. Legacy systems slow things down. Workarounds have become standard operating procedure. Teams, and likely customers, feel the friction every day, even if it has been normalized over time.

In fact, an overwhelming majority of banks say legacy systems are holding them back. Ninety-two percent of banks say their current level of legacy systems give them pause according to a 2025 Global State of Business Banking survey from FIS and TechStudio.

Very few leaders believe they are truly ahead when it comes to digital transformation. What’s more, CCG Catalyst found that many institutions are allocating increased tech budgets to incremental improvements on legacy platforms rather than genuine modernization.

Institutions are trapped in a cycle of investing around the edges. Incremental improvements feel safer. They show progress without introducing too much disruption. But, the underlying capability gap continues to grow.

Over time, those investments start to stack in the wrong direction. More effort goes into maintaining what already exists than into building what is needed next. Eventually, that cycle breaks, and what felt like a controlled delay turns into a scramble to catch up.

Why 2026 is the inflection point for digital lending transformation

That scramble is already starting.

Rate movement is reopening parts of the market that have been quiet, especially around refinance and new originations. The lenders best positioned to capture that demand are not reacting in real time. They already built the infrastructure to move when conditions changed.

At the same time, borrower expectations have settled into something much more defined. Speed, clarity, and digital access now shape how borrowers choose where to apply and who they stay with over time.

There is also a growing divide in how quickly institutions can respond. Some lenders are releasing new products and features in a matter of weeks. Others are still working through multi-month, or even multi-year, cycles just to make incremental changes.

That difference compounds quickly. It shows up in market share, growth, and customer retention.

This is what makes 2026 different. It is the point where delay stops being manageable and starts becoming visible.

Digital lending trends reshaping the competitive landscape

You can see this shift clearly in how lending itself is evolving.

Credit decisions are getting faster. In many cases, what used to take days or weeks is now happening in minutes. That speed goes beyond convenience. It fundamentally changes borrower behavior. When access to credit becomes immediate, expectations follow.

At the same time, lending is showing up in new places. Embedded lending is bringing financial products directly into the flow of everyday transactions. Instead of going to a lender, borrowers encounter credit options exactly where and when they need them. Bain and Company projects embedded finance will exceed $7 trillion in total U.S. financial transactions in 2026.

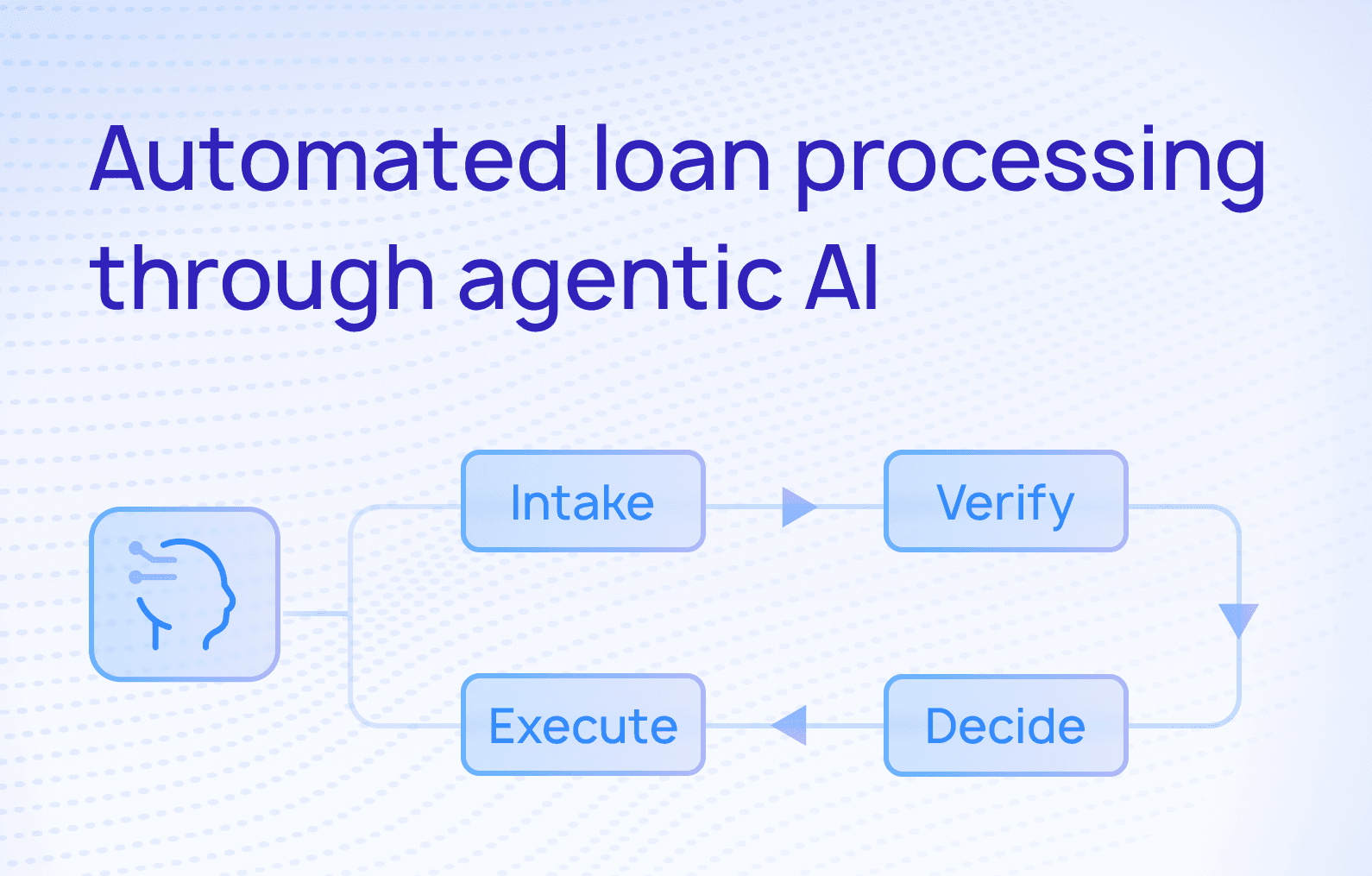

Behind the scenes, underwriting is also changing. More institutions are using alternative data and machine learning to expand access and refine risk decisions. These capabilities allow lenders to operate with a level of precision and flexibility that older systems were never designed to support.

Taken together, these shifts are redefining what “competitive” looks like in lending. It is less about who offers the product and more about how quickly, seamlessly, and intelligently that product can be delivered.

What digital transformation in lending actually means

At a practical level, digital transformation comes down to how a lending operation runs day to day.

In a modern environment, processes that once required manual intervention move automatically across the lifecycle. Data flows in real time instead of being stitched together after the fact. Teams spend less time navigating systems and more time making decisions.

Product development also changes. Instead of long cycles tied to rigid infrastructure, lenders can use modern bank lending technology to introduce new offerings, adjust terms, and respond to market shifts with much more flexibility.

From the borrower’s perspective, the experience becomes more consistent and transparent. Applications move faster. Communication is clearer. Servicing feels connected rather than fragmented.

For lending leaders, the biggest shift in your digital lending strategy is control. When systems are flexible and data is accessible, it becomes much easier to understand what is happening across the portfolio and to act on it.

The hidden cost of standing still

The impact of delaying your digital transformation shows up gradually but can have profound long-term implications.

A slower approval process means a borrower accepts an offer somewhere else. A clunky experience leads to a drop-off that never gets fully explained. A missed integration opportunity means losing visibility into a growing channel.

Over time, those moments add up. A majority of banking leaders (64%) say slow digital transformation has already cost them new customers. Many institutions are losing meaningful portions of their customer base due to poor experiences tied to legacy systems. At the same time, outdated data infrastructure increases exposure to regulatory issues, creating additional risk that is difficult to manage proactively. In fact, 68% of banks are susceptible to penalties at least once a year due to poor data quality within their firm, according to research from Gresham.

Operationally, the gap continues to widen. When one institution needs several months to launch a new feature and another can do it in weeks, the difference compounds quickly. McKinsey research found that large banks are 40 percent less productive than digital natives. On average, product rollout cycles take 4 to 6 months compared to fintechs and neobanks that release new product features every two to four weeks on average.

What may look like stability on the surface is often a slow erosion underneath.

What a real digital lending transformation looks like

One of the reasons institutions hesitate is the assumption that transformation requires a complete overhaul. In reality, most successful digital lending transformation efforts are more measured.

They start by identifying where change will have the greatest impact and building from there. New capabilities are introduced alongside existing systems to augment current lending operations without fully ripping and replacing, allowing teams to improve performance without disrupting the entire operation.

By focusing on a composable architecture using a modern credit platform that layers on top of existing legacy systems, banks and credit unions can take a smarter, more targeted path to modernization.

Over time, this means bank lending technology becomes flexible and dependencies on legacy systems are reduced. As a result, the organization gains the ability to adapt without starting from zero each time. And, each step forward makes the next one easier.

Why most lending transformations stall — and what successful ones have in common

Even with the right intent, many digital lending transformation efforts lose traction. As McKinsey notes, only 30 percent of banks that have undergone a digital transformation report successfully implementing their digital strategy, and the majority fall short of their stated objectives.

This isn’t unique to lending or banking. Low digital transformation success rates have been true for most industries for many years. At LoanPro, we’ve partnered with more than 600 lenders on digital transformation and modernization efforts, both large and small. Clear patterns emerge in the strategies that succeed compared to those that stall:

A clearly defined scope. Rather than attempting to modernize the entire operation at once, successful digital transformation efforts prioritize specific areas where change will have an immediate and visible impact. Early progress builds confidence and creates internal momentum.

Phased augmentation, not wholesale replacements. Successful lenders also think in phases. They introduce new capabilities alongside existing systems, allowing the organization to adapt over time. This reduces risk and makes transformation feel manageable rather than disruptive.

Measurable outcomes. Successful transformations are anchored in outcomes the business can track, such as faster time to decision, reduced servicing costs, or improved borrower conversion and retention. These metrics create accountability and make progress visible. Without them, it becomes difficult to tell whether anything is actually improving.

Change management beyond technology. There is an operational reality that often gets underestimated. Technology changes are visible while process and organizational changes are not. Without alignment across the business and strong change management processes, even the right technology struggles to gain traction.

Organizational alignment. Transformation is not owned by a single team. It requires coordination across lending, operations, compliance, and technology. The institutions that move forward are the ones that keep those groups working toward the same outcomes.

Progress comes from making transformation tangible by breaking it into steps and proving value at each stage.

What a modern digital lending solution makes possible

When those elements come together, the impact of your digital lending transformation becomes visible across the business.

Digital lending software starts to show up as a performance driver. These improvements appear in how quickly products reach the market, how efficiently teams operate, and how consistently borrowers move through the lifecycle.

Product launches that once took months begin to move at the pace of the market. Operational efficiency improves as manual processes are reduced and teams spend less time working around system limitations. Borrower experiences become more predictable and easier to navigate, which strengthens retention over time.

There is also a shift in how the organization operates internally. With better data visibility, regulatory requirements become easier to manage proactively. Decision-making improves as teams have access to real-time information instead of relying on delayed reporting. The focus moves away from maintaining systems and toward driving growth.

These changes compound. Over time, they reshape how a lending business competes. Institutions gain the ability to respond to market conditions, introduce new products with confidence, and build stronger relationships with borrowers.

That is what modern lending infrastructure makes possible. It creates the flexibility to adapt and the foundation to grow in a market that is only becoming more competitive.

Leverage these 9 innovative lending strategies to jumpstart your digital lending strategy.