Loan management system vs. loan origination system: what's the difference?

If you've spent any time researching lending software, you've probably run into LOS and LMS used almost interchangeably. Sometimes in the same paragraph, sometimes even in the same sentence. That's understandable, since the two systems work closely together and often get bundled into the same conversation. But they handle different parts of the lending process, and understanding where one ends and the other begins makes it much easier to figure out what your lending operation needs.

Key takeaways

A loan origination system (LOS) manages everything that happens before a loan is funded: applications, underwriting, approval, and closing. A loan management system (LMS) takes over from there, handling servicing, payments, collections, and reporting for the life of the loan. The distinction is useful, but it isn't always a clean line. Many modern platforms combine both functions into a single system, which is part of why the terms get blurred so often in practice.

What is a loan origination system (LOS)?

A loan origination system, or LOS, is software that manages the front end of the lending process. That includes collecting borrower applications, verifying information, running credit checks, underwriting the loan, and issuing approvals or denials. Once a loan is approved and funded, its job is done and the loan moves on to servicing.

Quick note on the acronym: LOS almost always means loan origination system in lending software, but it occasionally shows up defined as loan operating system instead, which sounds closer to what an LMS actually does. That overlap is probably part of why the two terms get confused in the first place. If you're seeing conflicting definitions while researching, loan origination system is the standard usage across the industry.

An LOS typically handles:

- Application intake and document collection

- Credit checks and underwriting

- Approval decisions and compliance checks

- Funding and disbursement

Lenders that only need help with the front end of the process, like a mortgage broker managing a high volume of applications, often look at an LOS specifically rather than a broader platform. If you're comparing specific options, our breakdown of top loan origination software covers the leading platforms on the market.

What is a loan management system (LMS)?

A loan management system, or LMS, picks up where origination leaves off. It manages a loan for its entire lifecycle after funding, which usually includes payment processing, statement generation, customer communication, delinquency management, and reporting.

An LMS typically handles:

- Payment processing and scheduling

- Interest calculations and account maintenance

- Collections and delinquency workflows

- Compliance reporting and audit trails

- Borrower communication and self-service tools

Because servicing tends to span the longest portion of a loan's life, this is usually where the day to day operational work happens. A strong LMS is what keeps loans healthy, borrowers engaged, and portfolios compliant long after the original application is a distant memory. For a closer look at how these platforms work, our guide on what a loan management system is and our roundup of top loan servicing software both go deeper on the servicing side specifically.

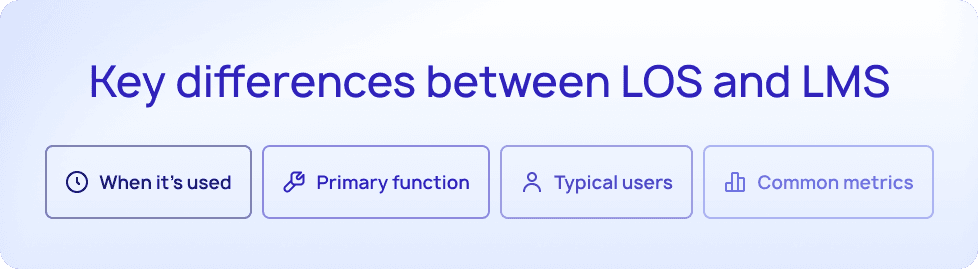

Key differences between LOS and LMS

At a high level, the split comes down to timing. An LOS is built for the period before a loan is funded. An LMS is built for everything after.

| Loan origination system (LOS) | Loan management system (LMS) | |

|---|---|---|

| When it's used | Before funding | After funding |

| Primary function | Application processing, underwriting, approval | Servicing, payments, collections, reporting |

| Typical users | Loan officers, underwriters, credit teams | Servicing agents, collections teams, compliance staff |

| Common metrics | Approval time, application volume, pull through rate | Delinquency rate, payment success rate, portfolio performance |

That framework holds up well as a starting point, but it's worth knowing it isn't a strict rule. Plenty of modern lending platforms combine origination and servicing into one connected system rather than keeping them as separate tools. When that happens, data flows between the two functions automatically instead of requiring a handoff, which is part of why some vendors describe their software with both terms depending on which capability they're highlighting.

Do you need an LOS, an LMS, or both?

The right answer depends on where your lending program actually needs the most support.

If you're mainly focused on getting more applications processed quickly and accurately, and you already have a system in place for managing loans after funding, a dedicated LOS might be the right fit. Mortgage brokers and lenders with a narrow, high volume front end often fall into this category.

If your challenge is on the other side, managing an existing portfolio, keeping up with payments and collections, and staying compliant as loans age, an LMS focused on servicing is the better starting point.

Many lenders, especially those building or scaling a lending program from the ground up, end up needing both. In that case, a platform that handles origination and servicing together can save you from managing two separate systems, keeping data in sync manually, and troubleshooting handoffs between vendors. It's worth weighing that tradeoff early, since switching from two disconnected systems to one unified platform later usually means a bigger migration than starting there in the first place.

Find the right fit for your lending program

Understanding the distinction is the first step. The next is figuring out what to actually look for once you know which one (or both) you need. Our guides on evaluating loan origination software and evaluating loan management software walk through exactly that.

Have questions? Checkout our FAQ:

Is LOS the same as LMS?

No, though they're closely related and often used together. An LOS manages the process of getting a loan approved and funded. An LMS manages the loan afterward, through servicing, payments, and collections.

Can one platform handle both origination and servicing?

Yes. Many modern lending platforms combine origination and servicing into a single system, which keeps data connected across the full loan lifecycle instead of requiring a separate handoff between two tools.

Do I need an LOS system for mortgage lending specifically?

Mortgage lending often has origination requirements that differ from other loan types, like specific disclosures and closing processes. Some LOS platforms are built specifically for mortgage workflows, while others are more general purpose. It's worth confirming a system supports your specific loan type before committing to it.

What's the difference between an LMS and a core banking system?

A core banking system typically handles a much broader set of banking operations, like deposits and account management, while an LMS is focused specifically on the loan lifecycle. Some lenders use an LMS as their core system for lending, while others integrate it alongside a broader core banking platform.