Common mistakes when selecting loan management software

Why the right lending platform is critical for growth

Credit providers recognize the importance of choosing the right platform. Selecting a loan management system isn't just about technology, but a strategic choice balancing the needs of your current portfolio against your projected growth and what you anticipate in the future. The right platform becomes the foundation that accelerates growth, streamlines operations, and opens new market opportunities.

But the wrong choice?

It creates bottlenecks, compliance headaches, and costly migrations that drain resources just when you need them most. It can kill a product before it even launches, or worse, leave your product stranded in a system that can’t keep up with your growth. What seemed adequate might crumble under operational strain; what seemed a bargain might cost you your business in hidden expenses and operational inefficiencies.

The good news, however, is that most of these pitfalls are as avoidable as they are costly.

Mistake 1: Underestimating the total cost of ownership (TCO)

The biggest trap in loan management software selection is focusing exclusively on the initial price tag. It's like shopping for a used car—you might find a steal of a deal, but you should brace yourself for what's coming when you roll it off the lot. Bargain software may end up costing far more once you factor in the total cost of ownership.

Focusing only on the initial license fee

Most creditors start their software search with a budget in mind, which is sensible. But limiting your analysis to upfront licensing costs is like that suspiciously cheap car. Without factoring in the cost of getting it moving and then maintaining it, you’re only seeing a fraction of the ultimate price.

Implementation costs alone can dwarf licensing fees. You'll need system integration, data migration, staff training, and extensive testing—all of which require significant time and resources. Then come ongoing expenses: maintenance fees, support costs, upgrade charges, and the hidden cost of internal resources needed to keep everything running.

Consider the true story of a LoanPro client, who shall remain nameless: Before moving to LoanPro, they went with a more "budget-friendly" system. But after six months of implementation delays, they still hadn’t launched. They ultimately realized that the system simply couldn’t support their program, and that the mistake had cost them not only what they paid to the vendor, but also speed to market.

Switching to LoanPro, they launched in just three months.

Ignoring the hidden costs of manual processes

Leaning again on the used car analogy, sometimes the biggest cost isn't the repairs—it's the time spent broken down on the side of the road, waiting in the shop, or hopping out to push. Many lenders stick with outdated systems or cobbled-together solutions thinking they're saving money, but they're actually paying a massive opportunity cost through inefficiency.

Manual processes also introduce significant risk. Human error in loan calculations, payment processing, or compliance reporting can lead to regulatory fines, borrower disputes, and operational chaos. Meanwhile, your team spends valuable time on repetitive tasks instead of focusing on growth and customer relationships.

Looking at the sticker price for a system, remember that the true cost also includes overtime hours for month-end reconciliations, additional staff needed to handle operations, lost business due to poor customer experience, and the constant stress of wondering when the next manual error will surface.

Mistake 2: Ignoring features that are not yet critical

Growing lenders face a classic dilemma: do you choose a system that fits your current needs perfectly, or invest in capabilities you'll need tomorrow? Considering that even the smoothest migrations are nothing to balk at, the economics of the situation lean toward future-proofing, but many companies still opt for "right-sizing" their platform to today's requirements. It's a decision they almost always regret.

Choosing a system that can't grow with your portfolio

Platform migrations are not easy. Even at LoanPro, where we've helped 450+ creditors through portfolio migrations, we can confidently say they would all prefer having a single system that just keeps working with them rather than face the prospect of another migration.

The pain of outgrowing a platform extends far beyond the technical complexity of moving data. You're essentially rebuilding your entire operational foundation while trying to maintain business continuity. Staff need retraining, integrations must be rebuilt, compliance documentation requires updates, and borrowers experience service disruptions.

Smart lenders evaluate platforms based on where they want to be in three to five years, not where they are today. Can the system handle 10x your current loan volume? Will it support new product types you're considering? Does it offer the reporting and analytics capabilities you'll need as you mature? These questions matter more than whether the platform perfectly fits your current workflow.

Overlooking compliance guardrails and security protocols

Lending is one of the most regulated industries, and compliance requirements only grow more complex over time. Yet many lenders treat compliance features as nice-to-have additions rather than core requirements. This is a dangerous miscalculation.

A loan management system should provide safeguards against regulatory violations, not just reports that tell you when things have gone wrong. Ideally, it should be difficult if not impossible to violate regulations because built-in controls and automations stop you. The platforms that genuinely understand regulatory requirements in your market have built their compliance capabilities into the core system architecture.

Security deserves equal attention. Your platform will house sensitive borrower data, financial information, and proprietary business intelligence. A security breach doesn't just cost money, but also risks your reputation and regulatory standing. Ensure your chosen platform meets industry security standards and undergoes regular third-party audits.

Disregarding the need for a configurable, API-first platform

Modern lending operations require flexibility and integration capabilities that weren't necessary even five years ago. Today's lenders need systems that can adapt to changing requirements and connect seamlessly with other business applications.

API-first platforms enable real-time data sharing between systems, eliminating the data silos that plague traditional lending operations. Whether you're integrating with credit bureaus, payment processors, accounting systems, or customer relationship management tools, robust APIs make everything possible.

Configurability matters just as much. Your lending products, underwriting criteria, and operational processes are likely unique to your business. A rigid system that forces you to adapt your processes to its limitations will become a competitive disadvantage. Look for platforms that can be configured to match your business logic rather than forcing you to change how you operate.

Mistake 3: Making a poor vendor choice

Selecting loan management software isn't just about buying a product—you're choosing a long-term partner. The quality of that partnership will significantly impact your operational success and growth trajectory. Unfortunately, many lenders don't evaluate vendors with the same rigor they apply to software features.

Neglecting the quality of post-implementation support

Implementation is just the beginning of your relationship with a software vendor. Over the years, you'll need ongoing support for everything from routine questions to complex customizations. Poor support quality can create major operational bottlenecks when you can least afford them.

Evaluate support offerings carefully. What are the response time commitments? Do they offer multiple support channels? Can you reach knowledgeable technical staff, or will you be stuck in first-level support queues? Most importantly, talk to existing customers about their support experiences. A vendor's promises matter less than their track record.

Consider the vendor's expertise in your specific lending vertical. Consumer lending, commercial lending, and specialty finance each have unique requirements. A vendor with deep experience in your market will provide more relevant guidance and faster resolution when issues arise.

Risking vendor lock-in with inflexible data silos or bankruptcy-bound companies

Vendor lock-in creates dangerous dependency that can limit your options and increase costs over time. Some vendors deliberately make it difficult to leave by restricting data access, using proprietary formats, or building technical barriers to migration.

Ensure you maintain ownership and control of your data. Your loan data, borrower information, and operational history belong to you—and you should be able to access it in standard formats if you ever need to change platforms. Negotiate clear data export rights and test the vendor's data portability capabilities before signing.

There's another consideration many lenders overlook: vendor financial stability. Many new market entrants are not yet cash positive and instead rely on investor money to fund operations. While venture funding can accelerate innovation, it also creates risks for customers who depend on the platform for daily operations. What happens if funding dries up or investors push for an acquisition that changes the vendor's priorities?

Choose vendors with sustainable business models and proven financial stability. A financially sustainable platform provider offers greater assurance that they'll be around to support your long-term growth.

Mistake 4: Rushing the 'build vs. buy' decision

In a vacuum, we all recognize that the decision to build an LMS in-house or purchase from a vendor determines many of the hard limits your operation will face: the products you can launch, the processes you can streamline, and ultimately the experience you offer your customers are all predicated on the technical realities of the system your running on.

Yet many organizations approach this decision reactively, driven by immediate pain points rather than long-term strategic considerations.

Building in-house seems attractive when you have strong technical talent and unique requirements that off-the-shelf solutions don't address. The promise of perfect customization and complete control appeals to many lending executives. However, the reality of building and maintaining loan management software is far more complex than most organizations anticipate.

Consider the true scope of what you're building. A comprehensive loan management system includes origination workflows, servicing capabilities, payment processing, regulatory reporting, collections management, and integration with dozens of third-party services. Each component requires specialized expertise and ongoing maintenance. Are you prepared to build and maintain all of these capabilities while also running your core lending business?

The opportunity cost deserves equal consideration. Every hour your development team spends building internal tools is an hour not spent on competitive differentiation and customer-facing improvements. While competitors leverage proven platforms to accelerate growth, you'll be debugging payment reconciliation issues and building compliance reports.

That said, buying isn't automatically the right choice either. Evaluate vendors carefully against your specific requirements, ensuring they can support your unique business model and growth plans. The key is making this decision strategically, with full awareness of the trade-offs involved, rather than defaulting to whichever option seems easier at the moment.

How LoanPro's modern credit platform helps you avoid these mistakes

The mistakes outlined above aren't just theoretical problems—they're challenges we've helped hundreds of lenders navigate and overcome. LoanPro's modern credit platform was built specifically to address the pain points that trap lending companies with inadequate technology solutions.

Trusted by Lending Leaders with a Proven ROI

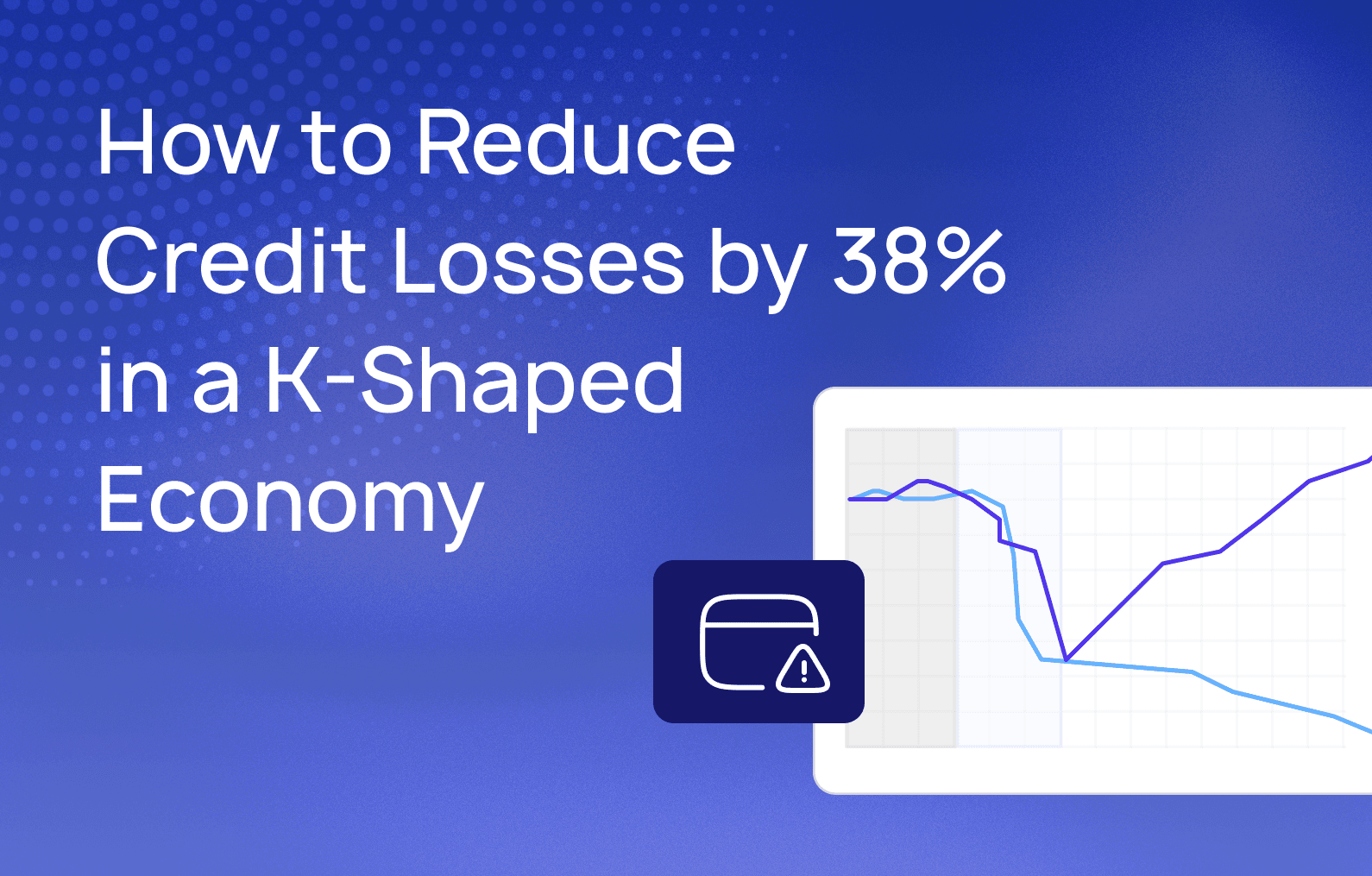

When evaluating total cost of ownership, transparency matters. LoanPro customers see an average 38% decrease in credit losses, driven by better data visibility and automated risk management capabilities. More importantly, our transparent pricing model eliminates the hidden costs that plague many lending platforms. You'll know exactly what you're paying for, with no surprise fees or costly add-ons required for basic functionality.

Our customers consistently report faster implementation times and lower ongoing operational costs compared to previous solutions. This isn't just marketing speak—it's the result of architectural decisions made specifically to reduce complexity and total cost of ownership.

Built for scale, security, and compliance

LoanPro's platform grows with your business, supporting everything from startup lenders to multi-billion-dollar portfolios. Our API-first architecture enables seamless integration with your existing systems while providing the flexibility to adapt as your requirements evolve.

Security and compliance are built into the platform foundation, not bolted on as afterthoughts. We maintain SOC 2 Type II certification and undergo regular third-party security audits. Compliance guardrails help prevent regulatory violations, while automated reporting reduces the manual effort required for regulatory submissions.

The platform's configurability means you can maintain your unique competitive advantages while leveraging enterprise-grade infrastructure. Whether you're launching new lending products or expanding into new markets, the system adapts to support your growth rather than constraining it.

A true partnership for long-term success

Choosing LoanPro means partnering with a team that understands lending operations inside and out. Our support organization includes former lenders, compliance professionals, and technical experts who can provide guidance beyond basic troubleshooting.

We maintain financial sustainability through profitable operations rather than venture funding dependency, providing stability you can count on for long-term planning. Our proven track record with 600+ lenders demonstrates our commitment to customer success across diverse lending verticals and business models.

Most importantly, we design our platform and partnerships to grow with you. As your business evolves, our platform capabilities and support organization scale to match your changing needs. You'll never outgrow LoanPro—instead, you'll discover new ways to leverage the platform's capabilities as your business matures.

Ready to see how LoanPro can transform your lending operations? Request a demo to see our configurable, API-first platform in action, or explore our case studies to see how 600+ lenders scale with LoanPro. For a deeper dive into the strategic considerations around platform selection, read our comprehensive guide on making the right build vs. buy decision for your credit platform.